Setting up a Business in India for Foreign Companies

Preamble

Given India’s rapidly growing market, the country’s investment potential has enticed a slew of foreign companies to establish their presence in India. Over the last few years, initiatives have been taken to ensure that establishing a business in India is more straightforward and foreign companies are encouraged to invest in the country.

Foreign investment in India is governed by the Foreign Direct Investment (FDI) policy announced by the Government of India and the provisions of the Foreign Exchange Management Act (FEMA) 1999. The Reserve Bank of India (RBI) has issued a notification which contains the relevant regulations. Foreign investment is freely permitted in almost all sectors. Foreign Direct Investments (FDI) can be made under two routes—the Automatic Route and the Government Route. Under the Automatic Route, the foreign investor or the Indian company does not require any approval from the RBI or the Government of India for the investment. Under the Government Route, approval by the Foreign Investment Promotion Board (FIPB), the inter-ministerial body responsible for processing FDI proposals and making recommendations for Government approval, is required.

Prohibited areas

Foreign investment in any form is prohibited in a company, a partnership firm, a proprietary concern or any entity, whether incorporated or not (such as Trusts) which is engaged, or proposes to engage, in the following activities:

- Business of a chit fund, or

- A nidhi company, or

- Agricultural or plantation activities, or

- Real estate business, or construction of farm houses, or

- Trading in Transferable Development Rights (TDRs).

Please note that real estate business does not include the development of townships, construction of residential/commercial premises, roads or bridges. To further clarify, partnership firms/proprietorship concerns having investments as per FEMA regulations are not allowed to engage in the print media sector.

In addition to the above, investment in the form of FDI is also prohibited in certain sectors such as:

- Retail trading.

- Atomic energy.

- Lottery business.

- Gambling and betting.

- Agriculture (excluding floriculture, horticulture, development of seeds, animal husbandry, pisiculture and cultivation of vegetables, mushrooms etc. under controlled conditions and services related to agriculture and allied sectors) and plantations (other than tea plantations).

Mode of Investment

Indian companies can freely issue equity shares / convertible debentures and preference shares subject to valuation norms prescribed under FEMA regulations. Issue of other types of preference shares such as non-convertible, optionally convertible or partially convertible are considered debt. As such, the guidelines applicable for External Commercial Borrowing (ECB), viz. eligible borrowers, recognised lenders, amount and maturity, end use stipulations and so on, will apply to such issues. Since these instruments are denominated in rupees, the rupee interest rate will be based on the swap equivalent of the London Inter-Bank Offered Rate (LIBOR) plus the spread permissible for ECBs of corresponding maturity. As far as debentures are concerned, only those which are fully and mandatorily convertible into equity, within a specified time would be reckoned as part of equity under the FDI Policy.

Business Structure Allowed

We look at a few important facets of available structures in India.

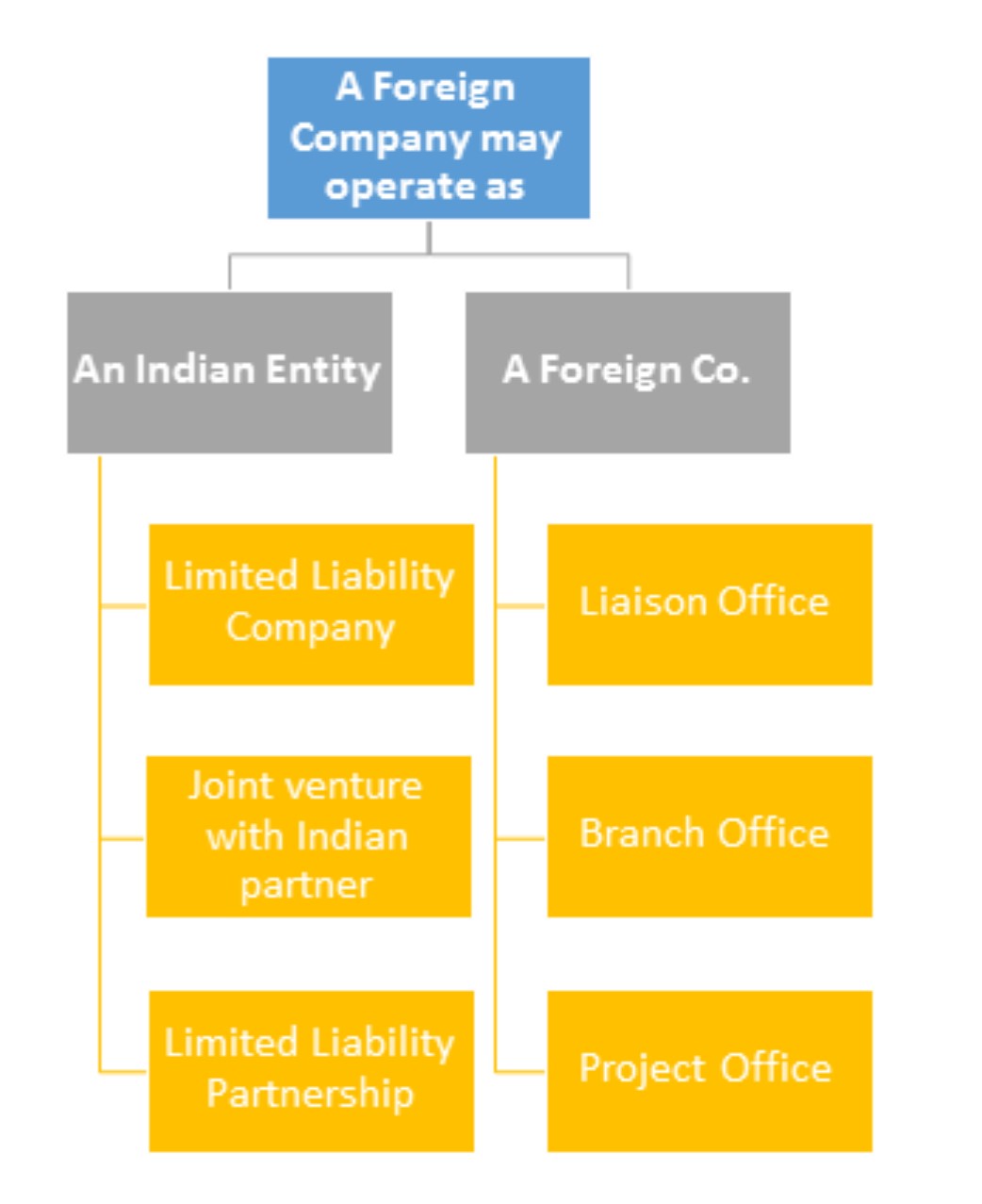

A foreign company can begin to establish a business in India by incorporating/registering or by establishing a liaison, project or branch office in India. To have a permanent establishment in India, a foreign company or national can either form a private limited company in accordance with the Act or form a limited liability partnership as per the provisions of the Limited Liability Act, 2008.

Following are the entry strategies for foreign companies to establish a legal presence in India:

Joint Ventures

Foreign companies can establish a business by forming a strategic partnership with business entities in India. International joint ventures have become essential wherein two business entities join forces to achieve a commercial objective. Joint ventures are becoming the ideal way to enter industries where 100% of FDI is not permitted in India.

Joint ventures are a relatively a low-risk route opted for by foreign companies wishing to enter the Indian market, provided these companies conduct appropriate due diligence on the Indian partners prior to forming an alliance. It allows the foreign investor to benefit from the Indian partner’s established market and consumers, distribution channels, local know-how and management.

Wholly Owned Subsidiary

By allowing foreign companies to establish wholly-owned subsidiary companies in India, the Indian market provides a convenient and beneficial business environment for these foreign entities. Foreign companies can set up wholly-owned subsidiaries by making 100% FDI in India through an automatic route (as defined previously) subject to the provisions of the Reserve Bank of India (RBI), Foreign Exchange Management Act, 1999 and the Act.

Requirements for Establishing a Company in India

Forming a new company provides flexibility and freedom as it can be structured in accordance with the requirements, objectives and obligations of both parties. A private limited company must have at least 2 (two) shareholders, while a public company should have at least 7 (seven) shareholders. Under the Act, it is a mandate that at least one director of every company is a resident of India [any person who has lived in India for more than 186 (one eighty-six) days is considered an Indian resident]. For a company to be registered, it must have an address in India. The legal jurisdiction applicable to the company will be determined by the city in which the company’s registered office is located.

Foreign companies can choose to establish a company with three directors, two being foreign nationals from the parent company and as a legal mandate, one being an Indian citizen. Further, as there is no requirement for minimum shareholding by the Indian director, foreign companies or nationals have the freedom to hold 100% of the shares of the Indian company.

Branch Office

For a foreign company to establish a temporary presence in India, a branch office is an effective strategy. The branch office is an extension of a foreign company and can engage in commercial business as a representative of the parent company.

Businesses keen on setting up a branch office should meet the following criterion as prescribed by the RBI:

- The applicant must be a body corporate incorporated outside India;

- The net worth of the parent company must not be less than USD 100,000 or its equivalent;

- The parent company should have a profit-making record during the immediately preceding five financial years in the home country.

Once established with the prior approval of the RBI, a branch office may remit profits of the branch outside India, subject to RBI guidelines and applicable taxes. Companies incorporated outside of India that are involved in manufacturing or trading are permitted to set up branch offices in India with the prior approval of the RBI. These branch offices are allowed to represent the parent company in India and carry out activities including, but not limited to, the following:

- Export/import of goods.

- Rendering professional or consultancy services.

- Promoting technical or financial collaborations between Indian companies and parent companies.

- Representing the parent company in India and acting as buying/selling agent in India.

Liaison Office

A liaison office serves as a communication link between the parent company, principal place of business or head office and entities in India, but it does not engage in any commercial, trading, or industrial activity, either directly or indirectly, and is restricted to gathering and providing information to potential Indian consumers.

Businesses wanting to set up a liaison office should meet the following criterion as prescribed by the RBI:

- The applicant must be a body corporate incorporated outside of India.

- The net worth of the parent company must not be less than USD 50,000 or its equivalent.

- The parent company should have a profit-making record during the immediately preceding three financial years in the home country.

Liaison offices are not allowed to undertake any business activity or to earn any income in India. The expenses of liaison offices are covered through inward remittances of foreign exchange from the head office outside India.

Project Office

As the name suggests, project offices are established by foreign companies to execute specific projects as per contracts to represent the parent company’s interests in India.

The RBI has granted general permission to foreign companies to establish project offices only if they have secured a contract, to execute a project in India, from an Indian company and subject to the following conditions:

- The project is funded directly by inward remittance from abroad; or

- The project is funded by a bilateral or multilateral international financing agency; or

- The project has been cleared by an appropriate authority; or

- A company or entity in India awarding the contract has been granted a term loan by a public financial institution or a bank in India for the project.

The RBI has given general permission for setting up project offices in India if the above-listed criterion is met. However, if the listed conditions are not met, the foreign company must approach the RBI for approval.

Analysis of Differences Between Liaison Office, Branch Office & Wholly Owned Subsidiary

| Basis | Liaison Office [LO] | Branch Office [BO] | Wholly Owned Subsidiary (WOS) |

| Meaning | A Liaison Office [also known as representative office] can undertake only liaison activities i.e. it can act as a channel of communication between Head Office abroad and parties in India. It is not allowed to undertake any business activity in India and cannot have any income in India. | Companies incorporated outside India and engaged in manufacturing or trading activities are allowed to setup Branch Offices with specific approval by the RBI. Normally, the Branch Office should be engaged in the activity of the parent company. | An incorporated entity formed and registered under the Companies Act, 1956. It is a distinct legal entity, apart from its shareholders. |

| Constitution |

|

|

|

| Permitted Activities |

|

| As per its ‘main objectives’ stipulated in the Memorandum of Association subject to Indian regulations. |

| Criteria for set up |

|

| A private company is required to be incorporated with a minimum authorised & paid up capital of INR 100,000 and minimum two subscribers. No requirement of track record of parent company as shareholder |

| Typical Terms of approval |

|

| A private company is required to be incorporated with a minimum paid-up capital of INR 100,000 and minimum two subscribers. Broadly, it:

The conditions will be different for Public Limited Companies. |

| Time limit of approval | Normally 3 years from the date of approval. | Normally 3 years from the date of approval. | Until the company decides to close down. |

| Basic Registration | The following registrations / approvals will be required:

| The following registrations / approvals will be required:

| The following registrations / approvals will be required:

|

| Liabilities of parent company/Head office | Parent company’s liability is unlimited for all acts and omission of LO. | The liability of the Branch is unlimited. The assets of the parent company are at risk of attachment in case the liabilities of the branch exceeds its assets. | The liability of the Parent company is limited to the extent of its shareholding in the WOS. The assets of the foreign company are not subject to any attachments. |

| Permitted Incomes | The entire expenses of the LO in India will be met out of the funds received from Head Office through normal banking channels. There will not be any income of the LO. | The entire expenses of the BO in India will be met either out of the funds received from Head Office through normal banking channels or through income generated by it in India. | All income arising out of its business activities. |

| Indian Income Tax | Since there is no income accrual, there is no income tax. LO is required to file information in Form 49C with the Income Tax Department. | Since a branch office of a foreign company is taxed as a foreign company in India, it is taxed @ 41.2% or 42.23% if the taxable income exceeds INR 10,000,000 during any financial year (FY). | Any Indian company is taxed @ 30.90% or 33.99% if the taxable income exceeds INR 10,000,000 during any financial year (FY). |

| Payment of Dividend to Parent | Cannot pay dividend. | Dividend/surplus distribution to Parent is tax free subject to normal tax in India | Dividend can be paid & now shareholders need to pay tax. |

| Management | LO is managed by Authorised Representative, resident in India (Country Manager) | BO is managed by Authorised Representative, resident in India (Country Manager). | Minimum two directors (can be foreign national, no need to be resident in India). |

| Audit a. Statutory Audit | Financials would be liable for statutory audit by a chartered accountant. | Financials would be liable to statutory audit by a chartered accountant. | Financials would be liable for statutory audit by a chartered accountant. |

| b. Internal Audit | Not Applicable. | Not Applicable. | Applicable, subject to conditions. Paid up capital + free reserves exceeding certain limits. |

| c. Tax Audit | Not Applicable | Applicable for cases where turnover exceeds INR 4 million. Non compliance would result in a penalty @ 0.5 % of the total turnover or INR 0.1 million, whichever is the lesser amount. | Applicable in case of turnover exceeding INR 4 million. Non compliance would result in a penalty @ 0.5 % of the total turnover or INR 0.1 million, whichever is the lesser amount. |

| Transfer Pricing | Not Applicable | Applicable | Applicable |

| Annual Compliance a. Filing |

|

|

|

| b. Meeting | Not Applicable. | Not Applicable. | Board – One meeting per quarter. Shareholder – One meeting per year. |

| Remittance of Profit to Parent company | None, except upon closure of LO. | Profits can be freely repatriated to the Parent Company subject to payment of applicable taxes. |

|

| Borrowing | Not allowed | The BO is not allowed to borrow locally unless given prior approval by the RBI. |

|

Conclusion

Various factors are to be considered before choosing the best strategy for establishing a business in India including, but not limited to, the due diligence of the Indian partners, exit strategies, Indian laws and regulations, and operational issues such as connectivity, employment and state-wise regulations. Additionally, the preferred path for a foreign company to establish a presence in the Indian market will also depend on the company’s specific requirements, such as the size of its operations, expansion and commercial goals.

For any questions or advice about establishing a business in India as a foreign company, please get in touch with us at mumbai@ecovis.in.

CA R.L.Kabra

Chairman Emeritus

ECOVIS RKCA, India

Contact us:

ECOVIS RKCA Advisors Ltd.

1903, Kailas Business Park, Vikhroli (West), Off Powai400078 Mumbai

Phone: +91 22 220 44 737

www.ecovis.com/india